This morning’s Treasury auction revealed significant challenges in the 2-Year and 5-Year securities offerings, with the latter being particularly concerning. The auction for the 2-Year bonds was marked by a high yield of 4.138%, a notable increase from October’s 3.519% and the highest yield since June. Additionally, the auction experienced a tail of 1.6 basis points, marking this as the fourth consecutive auction where the securities failed to sell at a higher price than expected. Such a tail indicates a decrease in demand, with this instance being the second largest tail of 2024, following January’s slight 2 basis points tail. Although the bid-to-cover ratio was relatively stable at 2.39, this figure was the lowest since June, reflecting a cooling appetite among investors for these longer-dated notes.

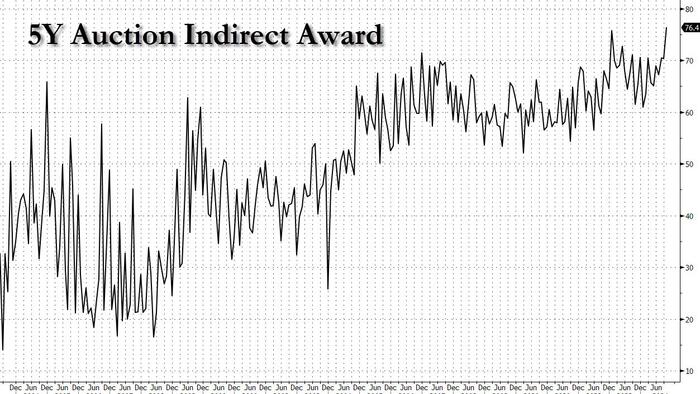

While the overall performance of the auction was disappointing, there was a notable increase in indirect bids, which accounted for 76.4% of the auction’s total, the highest percentage recorded to date. This increase suggests that despite the overall ugliness of the auction, international investors are still seeking opportunities in U.S. Treasury securities. This sharp rise in foreign interest came at the expense of direct bidders, whose share plummeted to just 9.5%, marking the smallest allocation for this group since December 2018. Dealers were left with a marginally reduced share of 14.2%, slightly below the recent auction average of 14.4%.

Nevertheless, the disparity in demand raises pertinent questions about future pricing and investor sentiment towards U.S. government bonds. The disconnection between the record high for indirect buyers and wider tails during these auctions suggests that while foreign investors may be willing to purchase bonds at current rates, domestic interest is waning. Consequently, this trend may exert upward pressure on yields, as seen in the 10-Year yield that edged back to nearly 4.30%. Such movements in yield indicate a tightening in financial conditions, which could further exacerbate stresses in the equity markets.

The reaction from the stock market could be significant as increasing yields generally lead to stiffer competition for capital, drawing funds away from equities and into bonds. Investors are now grappling with a more constrained environment, driven by rapid tightening amid concerns over inflationary pressures. The shift in the yield curve reflects broader economic uncertainties that could influence central bank policies in the near future, leading to enhanced volatility in both bond and equity markets.

The combination of these dynamics creates a complex landscape for financial markets moving forward. With the possibility of continued yield increases paired with fluctuating investor sentiment, market participants must carefully assess their strategies, particularly in equities, which may face downward pressure if bond yields continue to rise. Additionally, the evolving situation for Treasury auctions hints at potential liquidity concerns and a need for the Treasury to re-evaluate its approaches to bond sales in response to changing demand dynamics among both foreign and domestic investors.

In summary, the Treasury’s recent auction results underscore growing challenges within the fixed income space. Even as foreign interest appears to hold steady, the overall demand for U.S. bonds is increasingly mixed. The trends in pricing from these auctions, along with the implications for stock market performance, signal that careful observation of financial conditions is crucial. With rising yields shaping the outlook, market participants will need to remain agile, ready to adapt to a potentially more volatile market environment driven by the interplay of economic indicators and investor behavior.

")