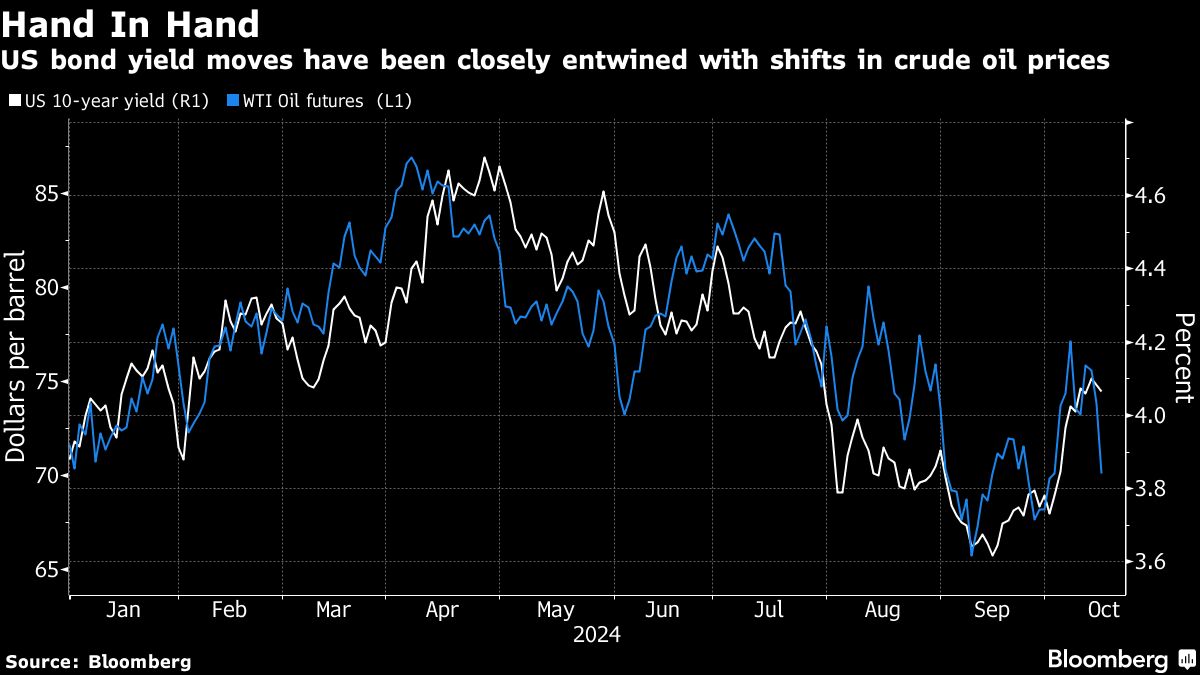

Treasuries experienced a significant rally, marking their most substantial gains in two weeks, as a drastic decline in oil prices helped alleviate concerns surrounding inflation. The yields on US 10-year Treasury bonds fell over five basis points to 4.05%, retreating from a high not seen in two and a half months. This downward trend in yields extended beyond the US, with Canadian government bond yields also decreasing sharply as the nation reported favorable consumer prices data. Additionally, most European bond markets saw a similar decline, indicating a broader shift in investor sentiment regarding inflation and interest rates.

Oil prices took a noteworthy plunge, dropping more than 5% to below $70 per barrel. This decrease followed reports suggesting that Israel might avoid targeting Iran’s crude infrastructure in retaliation for missile attacks. Such developments have contributed to a sense of relief among investors, who had been increasingly anxious about a potential resurgence of inflationary pressures driven by geopolitical tensions in the Middle East and the economic policies that could emerge from the upcoming US presidential election. According to Christoph Rieger, head of rates and credit research at Commerzbank AG, current market behavior suggests that many traders are closely monitoring oil futures, and this connection may not necessarily provide a clear indication of long-term inflation trends.

The fluctuations in crude oil prices have mirrored the tumultuous events unfolding in the Middle East, a region that accounts for a significant share of the world’s oil supply. Investors have reacted strongly to recent economic data, which has shown robust wage growth in the US as well as a higher-than-expected consumer price index (CPI) reading. This combination of factors has heightened fears of inflation reemerging in the US economy, reflecting concerns about ongoing price instability as geopolitical tensions persist. Observers are particularly attentive to how these dynamics might shape market expectations in the coming months.

Adding to the inflation narrative, a survey of 29 economists conducted from October 7 to 10 indicated that inflation is projected to exceed the Federal Reserve’s long-term estimates regardless of whether Donald Trump or Kamala Harris secures the presidency. These forecasts suggest persistent inflationary pressures are expected over the next four years, thereby influencing investment strategies and economic planning. This commentary on inflation expectations underscores how political outcomes may have ramifications on monetary policy and broader economic conditions in the US.

Canada’s recent consumer price index (CPI) data revealed a significant decline, as the year-on-year rate dropped to 1.6%, the lowest level recorded since February 2021. This outturn was larger than economists had anticipated, prompting a swift reaction in the Canadian bond market, where yields fell as investors re-evaluated their expectations of future inflation and interest rates. This trend reflects the interconnectedness of the North American economies and the ways in which economic indicators can swiftly influence bond markets across borders.

In conclusion, the recent rally in Treasuries, coupled with the sharp decline in oil prices, illustrates the significant interplay between global markets, inflation expectations, and geopolitical events. With ongoing uncertainties in the Middle East and fluctuating consumer price indices in both the US and Canada, investors remain vigilant in assessing the potential impact of these developments on future economic policies and market conditions. As central banks and policymakers respond to these evolving scenarios, the implications for interest rates, investment strategies, and economic stability will continue to be closely monitored.