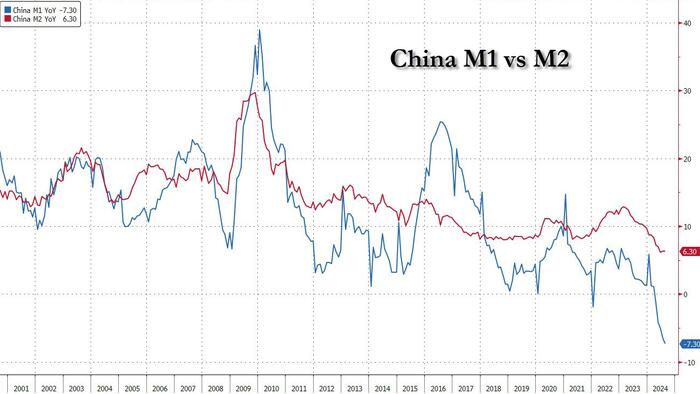

In a recent analysis, Borislav Vladimirov of Goldman Sachs presents a compelling argument regarding China’s impending need to activate quantitative easing (QE). His assessment builds upon observations that if the Chinese government fails to implement QE, the country’s monetary dynamics could face severe challenges. Specifically, he highlights the crucial relationship between M1 and M2 money supply, indicating that a stagnation of M1 growth relative to M2 could lead to significant repercussions. Under such circumstances, the government might distribute monetary inefficiencies among the weaker segments of the economy. This could exacerbate existing economic divisions, as affluent corporations and households are likely to save any financial stimulus rather than reinvest it, thus throttling economic multipliers.

The ramifications of avoiding QE are noteworthy. Vladimirov warns that the absence of aggressive monetary intervention could set the stage for an economic crisis in China within the next 12 to 18 months. The concern rests on the potential for what he describes as “global deflationary destruction,” where stagnant growth and insufficient monetary circulation lead to a marked contraction in economic activity. Collectively, these factors threaten to diminish domestic consumption and overall economic vitality, resulting in broader implications not only for China but for the global economy.

Conversely, should China choose to embrace QE, the resulting economic environment might shift dramatically, leading to increased asset prices across various sectors. For instance, a deliberate activation of QE could propel oil prices upwards, reflecting heightened demand driven by newfound liquidity in the market. Moreover, alternative assets such as Bitcoin and gold would likely experience substantial price surges as investors seek refuge from inflationary pressures and currency devaluation. This scenario suggests that the activation of QE may ignite a broader “reflationary tsunami” that could alter the global economic landscape significantly.

Goldman’s insights draw attention to the delicate balance that China must maintain to navigate its complex economic structure successfully. As one of the largest economies in the world, its monetary policy decisions often reverberate internationally. Thus, the implications of China’s quantitative easing extend beyond its borders, potentially influencing commodity prices, currency values, and the investment climate in various markets globally. Investors, therefore, must remain vigilant and consider how macroeconomic policies, particularly in China, can affect their portfolios.

China’s decision to implement QE or refrain from it ultimately hinges on the broader economic indicators at play, including inflation rates, domestic demand, and the global economic outlook. The nuanced analysis provided by Vladimirov serves as a reminder of the interconnectedness of current economic policies and emphasizes the critical role that central banks play in steering the path toward recovery or recession. The outcomes of such decisions will likely manifest through economic growth patterns, consumer behavior, and the stability of financial markets around the world.

In conclusion, the arguments laid out by Borislav Vladimirov underscore a pivotal moment for China regarding its monetary policy approach. The potential activation of QE represents a fork in the road that could dictate the health of both the Chinese economy and the broader financial system in the coming years. Recognizing the risks associated with inaction, as well as the promising opportunities presented by QE, is essential for stakeholders seeking to understand the future trajectory of both China’s economy and the global market. As investors anticipate these developments, careful consideration of the interplay between monetary policy, asset prices, and economic growth will be crucial in adapting strategies and making informed decisions in this ever-evolving economic landscape.

")