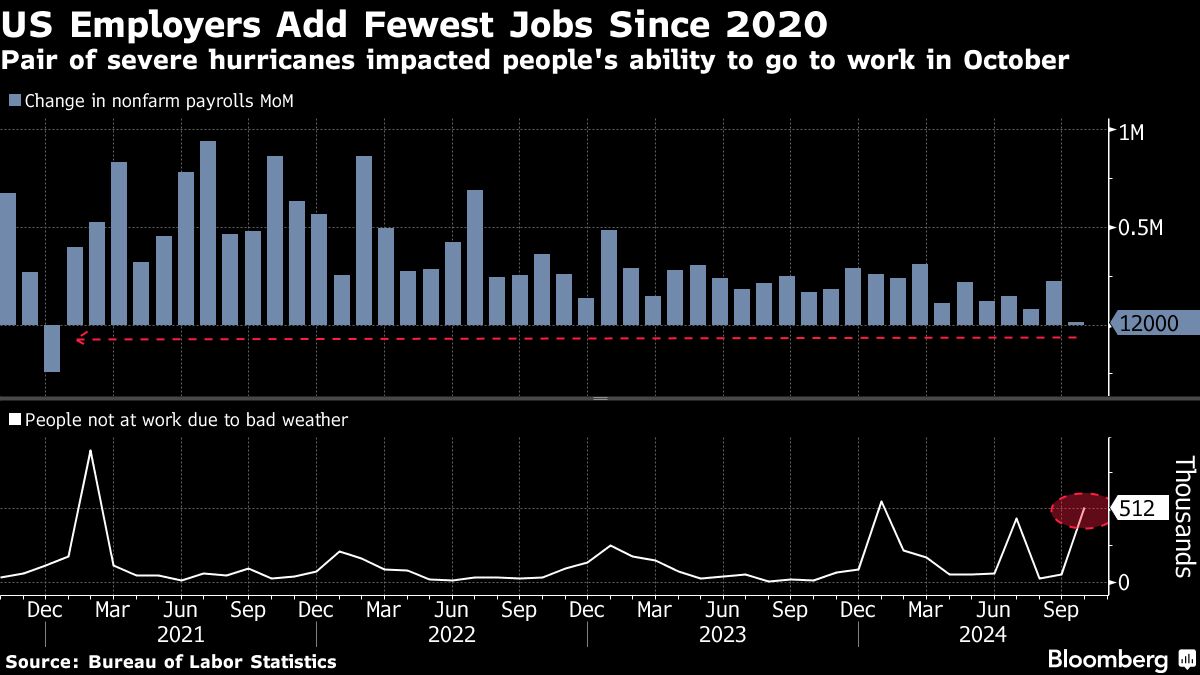

In October, a lackluster employment report indicated only a modest increase of 12,000 nonfarm payrolls, raising expectations that the Federal Reserve will proceed with a quarter-point interest rate cut during their upcoming meeting. While this figure was influenced by factors such as hurricanes and a significant strike at Boeing, revisions to previous months revealed weaker hiring trends in August and September. The unemployment rate remained unchanged at 4.1%, suggesting a labor market that is gradually downshifting from the peak levels experienced in previous years. This situation reinforces the argument for the Fed to continue reducing its restrictive rate policies aimed at curbing inflation.

Market analysts, including Steven Blitz from TS Lombard, conclude that this report all but ensures a 25-basis-point cut in both November and December. He predicts that the Fed will lower rates to between 4% and 4.25%, a notable reduction from the current benchmark rate, as a response to the revised weaker job figures from August and September. The combination of declining job openings and stagnant economic activity, as reported in the Fed’s Beige Book, supports the idea that the economy is showing signs of cooling off, thus justifying a more accommodative monetary policy.

Despite concerns reflected in the employment data, some central bank officials advocate for a gradual approach to interest rate cuts. The third quarter of the US economy grew at an annualized pace of 2.8%, primarily driven by robust consumer spending. This expansion has led to mixed feelings among policymakers, who are split between wanting to lower rates to foster further growth and being cautious in their approach given the current strength of the economy. The prevailing consensus is leaning towards a quarter-point reduction in rates during the next Federal Open Market Committee (FOMC) meeting post-election, in line with futures markets’ predictions.

The Bureau of Labor Statistics (BLS) acknowledged the complicating effects of Hurricanes Helene and Milton on payroll estimates for various sectors, although it remains uncertain how significantly these storms impacted the results. Nonetheless, analysts view the labor market as fundamentally healthy, citing consistent gains in both employment levels and labor supply over the year. Josh Hirt from Vanguard remarked that despite temporary setbacks, the employment landscape still reflects overall robust conditions.

This month’s employment data, while less than favorable, does not alter the Fed’s long-term strategy, which aims to keep inflation in check while fostering economic growth. Policymakers’ approach to rate cuts has been characterized by a desire to balance economic vitality with inflationary control. As the labor market continues to show signs of moderation, the Fed appears to be positioning itself for a more accommodative stance to alleviate potential economic weaknesses without prematurely stoking inflation.

In summary, the weak October employment report combined with earlier downward revisions creates a compelling case for the Federal Reserve to proceed with interest rate reductions. Despite some challenges, economic indicators signal a reasonably healthy labor market, which allows the Fed to navigate its monetary policy decisions carefully, weighing the risks of a slowing economy against the need for ongoing inflation management. The upcoming meetings will likely reveal how the Fed balances these competing priorities in an evolving economic landscape.