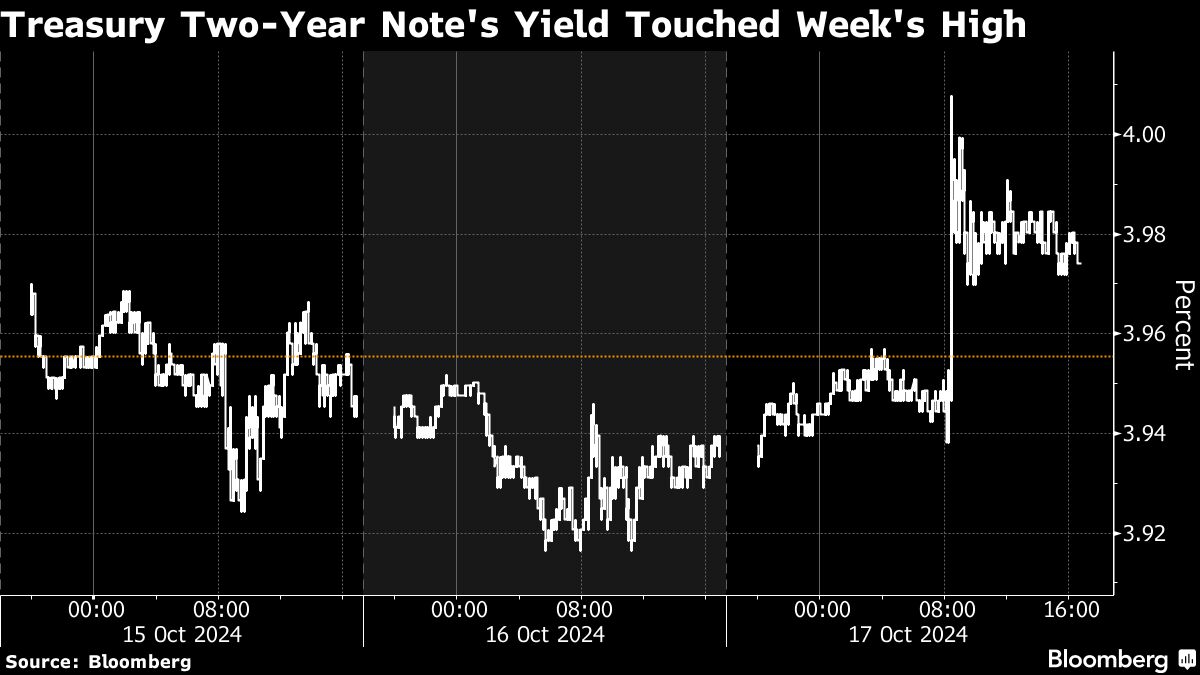

A recent selloff in Treasuries has had a significant impact on financial markets, leading to a strengthened US dollar and a mixed performance in equities. Traders have adjusted their projections for US interest rate cuts after fresh indicators of economic strength emerged, including robust retail sales data from September that surpassed expectations. Following this, US futures trended slightly higher after the S&P 500’s record-breaking performance earlier in the week, ending the session with minimal changes. The adjustment in financial forecasts was also accompanied by rising Treasury yields, prompting an increase in the index measuring dollar strength to levels not seen since early August. This morning, Australian and New Zealand bond yields mirrored these rising trends.

The stronger-than-anticipated economic data, particularly in consumer spending, appears to have altered market sentiment regarding the Federal Reserve’s potential actions in coming meetings. While some analysts suggest there is a “narrow path toward a Fed pause in November,” it hinges on continued strong economic indicators, with most expectations now shifting towards a longer-term outlook of elevated interest rates beyond 2025. The recent reports, including a robust jobs summary and higher inflation metrics earlier this month, reinforced the notion that a recession is not on the immediate horizon for the US economy.

In Asia, market participants are keenly awaiting China’s GDP data for the third quarter, which is anticipated to reveal a slowdown in growth—the most sluggish in six quarters. Additional metrics, such as home prices, industrial production, and retail sales are also expected, providing necessary insight following the economic support measures announced recently in China. These developments have caused volatility in Chinese equities as investors wrestle with the broader implications for the economy. Also noteworthy is the situation in Japan, where inflation numbers met expectations but placed the yen under pressure, raising concerns about possible government interventions as it passed the critical 150-per-dollar threshold.

Corporate performance in the US saw notable movements, particularly in the tech sector. Shares in Taiwan Semiconductor Manufacturing Co. soared to all-time highs after the company outperformed expectations and increased its revenue projections for 2024. This positive momentum extended to stocks like Nvidia, which also experienced gains, and Netflix, which reported subscriber growth exceeding estimates. Conversely, Elevance Health faced difficulties with an 11% drop in its stock price following a reduced annual outlook against the backdrop of a tripled profit in Travelers Cos., highlighting the mixed nature of corporate earnings.

Strengthening economic indicators have driven Citigroup’s Economic Surprise Index to its highest level since April, which gauges the difference between actual economic releases and market predictions. Financial experts like Ellen Zentner from Morgan Stanley view this trend as a confirmation of the economy’s robustness, suggesting that the Federal Reserve may face upward pressure against rate cuts in November. Patrick Roach from LPL Research points to a solid growth trajectory in consumer spending during September, prompting observations on the potential challenges facing the job market. The consensus view among analysts leans toward expectations of at least a modest rate cut still being on the table.

On the commodities front, gold prices have surged amidst ongoing tensions in the Middle East, establishing a new record. Additionally, West Texas Intermediate crude oil prices have edged upward and are approaching the $71-per-barrel threshold as global demand factors continue to play a role in price movements. Important data releases on the horizon include China’s GDP on Friday, US housing starts also due on the same day, and speeches from Federal Reserve officials that could provide further insight into the central bank’s stance going forward. Overall, the financial landscape is marked by cautious optimism as economic data continues to guide investor sentiment and market dynamics.